Searching financial statements for ESG disclosures is often frustrating. The information is scattered across lengthy 10-Ks, annual reports, and even buried in footnotes. Furthermore, terminology is inconsistent. One company might reference “carbon emissions,” another might call it “greenhouse gases,” while others bury environmental risks under broad “regulatory compliance” language. Analysts run multiple CTRL-F searches with different terms, flipping through dense sections, then manually piece together fragments to form a complete picture. This lack of standardization not only slows down equity research but also increases the risk of overlooking critical information. Key details about environmental liabilities, pending litigation, or climate-related risks may materially impact the business.

Why ESG Disclosures Are Hard to Track

Regulations require companies to disclose ESG events, but the language is inconsistent and often buried deep in filings. Analysts need a working set of terms and phrases to catch these variations and make sure ESG risks aren’t missed.

A Reuters commentary underscores how the lack of standardized, high-quality environmental data complicates emissions disclosures, especially for financial institutions. The article illustrates a “chicken-and-egg dilemma.” Companies delay emissions calculations until better data exists. Yet without early reporting, many gaps persist. Variations in data collection methods, industry differences, and regional standards further erode reliability. To bridge these gaps, the text emphasizes using estimation techniques. The text also contains strategic data repositories (e.g., the Partnership for Carbon Accounting Financials). The text encourages collaborations between public and private sectors to improve data collection and transparency.

Restatements and Reliability Issues

An analysis by Deloitte found that nearly half of FTSE 100 firms had to restate their climate-related scores. This was primarily due to changes in data collection or corrections to past errors. Scope 3 emissions—indirect emissions from activities like business travel or waste—were particularly problematic. Such restatements show a commitment to accuracy. But they also reveal that ESG metrics are more prone to revision than financial figures. The main reason is immature reporting practices and evolving methodologies.

In 2019, the International Institute for Sustainable Development (iisd.org) identified three core challenges in ESG reporting. They are complexity and reporting burden, lack of comparability, and inconsistent methodologies across frameworks. The study notes that many companies struggle to select the right standard, apply materiality, and align reporting across metrics. This creates incoherent disclosures that are hard for investors to compare. These challenges explain why retrieving accurate ESG information from financial statements is still slow, inconsistent, and frustrating.

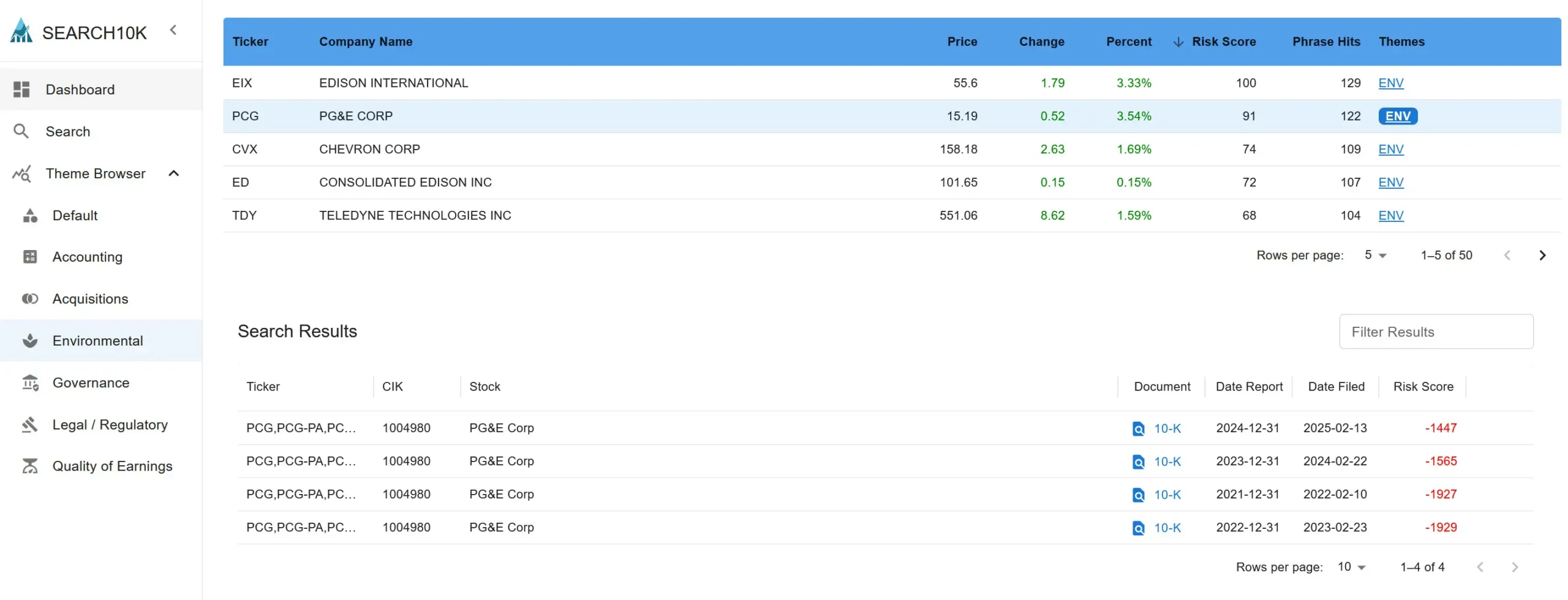

How Search10K Simplifies the Process

Search10K provides you the themed phrases to not only bring out the results that match, but also to rank companies based on their underlying document scores. It’s the prioritization that helps cut through the tediousness of manual searching.