Two of the market’s biggest AI names, compared side by side using nothing but their own filings. No analyst targets, no forecasts.

Sources: NVIDIA and Meta SEC filings and earnings releases, linked throughout. Updated July 2026. For informational purposes only; not investment advice.

If your portfolio owns both NVIDIA and Meta, you probably feel nicely diversified. One makes chips, the other runs social apps. Look a little closer, though, and they’re more similar than you think, almost two sides of the same coin. NVIDIA makes the chips; Meta’s one of the biggest buyers of them anywhere. The giveaway sits in the filings: for years, NVIDIA has kept its two biggest customers anonymous, calling them only Customer A and Customer B, together with more than a third of its revenue. So when its fiscal 2026 results openly spelled out a multiyear deal to sell Meta millions of GPUs, that was a real change in tack, and now a big slice of Meta’s AI spending loops straight back into NVIDIA’s revenue. That’s the thread worth pulling, because holding both isn’t quite the two-way bet it looks like. Let’s flip the coin over and study both faces, using only the companies’ own filings and disclosures, and see what that says about each business.

Supplier and Customer, One Boom

Start with the two faces, because everything else follows from them.

NVIDIA’s Story

First and foremost, NVIDIA is the supplier, a fabless chip designer that pioneered the GPU and leaves the manufacturing to TSMC. Back in 1999 it shipped what it billed as the world’s first GPU, a chip built to draw game graphics, and for years PC gaming and the entertainment industry were its bread and butter.

The turn came in 2006, when NVIDIA released CUDA and let developers use those graphics chips for general number-crunching. That converted a gaming part into a parallel-computing engine, and NVIDIA has surfed one wave of demand after another since: gamers first, then a boom-and-bust run of crypto miners around 2017 and 2021, and now AI.

Its customer base has moved with each wave. Where it once sold mostly to gamers, board makers, and PC builders, its biggest buyers today are the hyperscalers, cloud providers, and AI model makers racing to train ever-larger models. Data center is now about 90% of revenue; gaming, still a real business at $16 billion, has gone from the main event to a supporting act.

Meta’s Story

Meta stands on the other side of that transaction, and it’s worth being precise about what it’s buying all those chips for. It runs Facebook, Instagram, WhatsApp, and Messenger, turns the attention of more than 3.5 billion daily users into ad revenue, and now pours that money into AI.

That work is consolidated inside Meta Superintelligence Labs, the group it built around its $14.3 billion Scale AI stake and staffed to chase what Zuckerberg calls “personal superintelligence.” The lab isn’t some side quest to bankroll the VR division, either. It points straight at Meta’s core business. Better models sharpen ad targeting and recommendations, which is what moves revenue, and they power the Meta AI assistant, now past a billion monthly users, along with its Ray-Ban smart glasses.

Advertisers, Meta’s real customers, also get more for their spend, while its open Llama models, which Meta says have passed a billion downloads and run in production at the likes of Spotify, AT&T, and DoorDash, pull the wider developer world onto Meta’s stack. Cloud hosts even pay Meta a cut of what they earn serving those models.

The millions of GPUs NVIDIA just agreed to sell Meta feed exactly this machine: one company’s capital budget is the other’s order book. Same coin, two faces, and from here their numbers start to diverge.

THE MATCHUP AT A GLANCE

| Metric | NVIDIA (NVDA) | Meta (META) |

| Latest fiscal year | FY2026 (ended Jan 2026) | FY2025 (ended Dec 2025) |

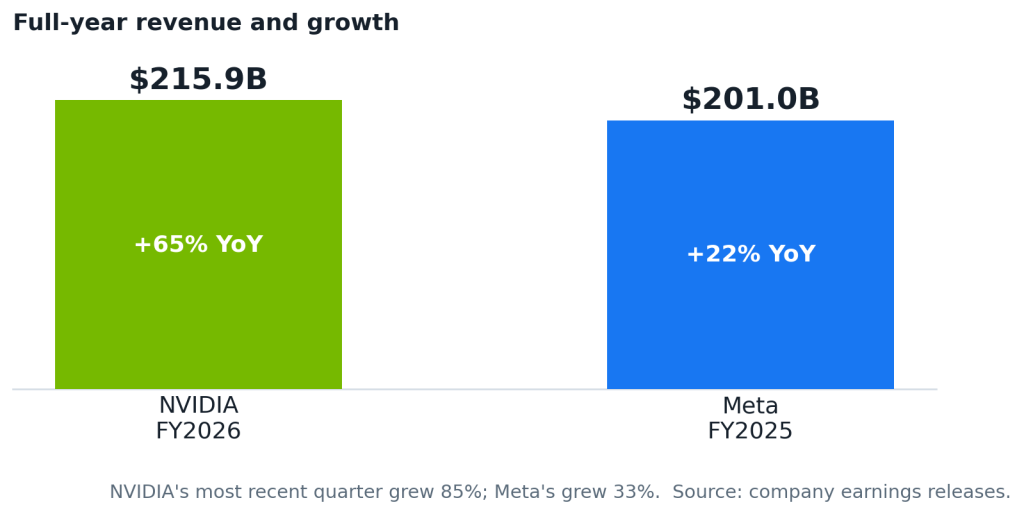

| Revenue / YoY growth | $215.9B / +65% | $201.0B / +22% |

| Most recent quarter | $81.6B / +85% | $56.3B / +33% |

| Gross margin | 71.1% | 82.0% |

| Operating margin | 60.4% | 41.4% |

| Net income | $120.1B | $60.5B |

| Free cash flow (margin) | $96.6B (45%) | $43.6B (22%) |

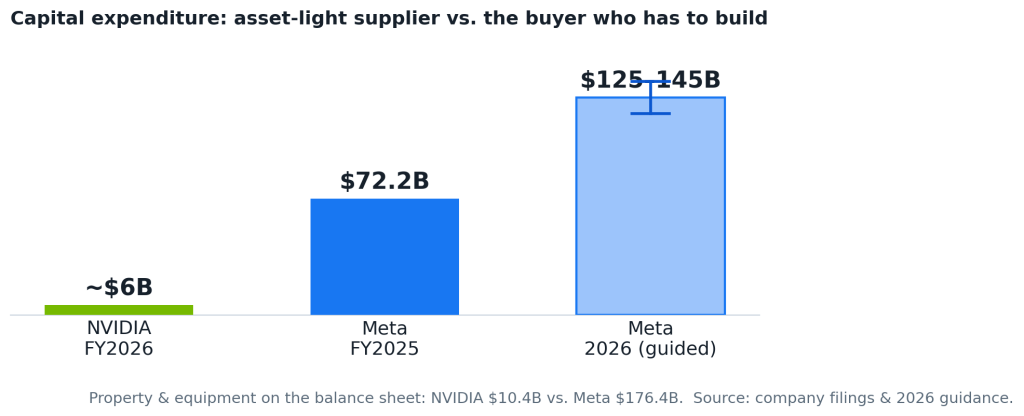

| Capital expenditure | ~$6B (fabless) | $72.2B |

| 2026 capex plan | Minimal (fabless) | $125B to $145B (guided) |

| Capital returned, latest FY | $41.1B | $31.6B |

| R&D (% of revenue) | $18.5B (8.6%) | $57.4B (28.5%) |

| Core moat | CUDA + full-stack platform | Social graph, 3.5B+ daily users |

A Supplier’s Spike, a Platform’s Compounding

The first place they split is growth, and the gap is enormous.

NVIDIA grew fiscal 2026 revenue 65% to $215.9 billion, with data center sales alone hitting $193.7 billion. Then posted 85% growth the very next quarter. Numbers like that don’t come from a great product alone; they come from scarcity. The world wants more AI compute than anyone can build, and NVIDIA’s the one selling into that scarcity. Yet while it’s real money, scarcity fades, and shortage-fueled growth fades with it.

Even though Meta’s 22% growth to $201.0 billion looks sleepy beside that, it’s the sturdier story: a mature ad machine that keeps getting sharper, with more impressions and higher ad prices rolling in through 2025 and into 2026. Advertisers keep paying up because the ads convert. Meta-commissioned research points to strong returns, often cited near $4 in sales for every dollar spent, though independent benchmarks run lower, closer to $2. Regardless, the money comes back, so buyers compete for finite inventory and bid the price higher. It all compounds on a base twenty years deep.

One face is growing because the world’s short of what it makes; the other because it keeps getting better at what it already does. Hold that difference, because it shapes everything downstream.

The Economics of Where You Sit

Downstream is the income statement, and here the two companies really show their true colors.

Meta earns an 82% gross margin because serving one more ad costs it almost nothing, about as good as economics gets. NVIDIA earns 71%, back to 75% by year-end once a China-related charge gets cleared, which is remarkable for a company shipping physical hardware.

However, margin isn’t the number that tells you about quality; cash is. NVIDIA turned 45% of revenue into free cash flow of roughly $97 billion, because it doesn’t own the factories or, increasingly, the data centers. Meta, on the other hand, converted about 22%. That share is also shrinking, because it has to build the very infrastructure NVIDIA sells.

What’s more, on similar revenue, NVIDIA cleared $120.1 billion of net income to Meta’s $60.5 billion. The seller keeps more of every dollar than the buyer, who has to pour the concrete.

Which raises the obvious question: what’s each one doing with all that cash? Opposite things, it turns out.

Harvesting the Boom vs. Betting on It

NVIDIA spent about $6 billion on capital projects last year and carries just $10 billion of property and equipment, so it handed $41 billion back to shareholders and authorized another $80 billion buyback in May 2026. It’s cashing the boom’s checks.

Meta’s doing the reverse, at a scale that’s hard to overstate: $72 billion of capital spending in 2025, $176 billion of property and equipment on the books, and 2026 guidance cranked up to $125 billion to $145 billion, nearly double last year and partly funded with new debt. And it isn’t only Meta: its closest rival, Alphabet, is spending even harder, guiding as much as $190 billion for 2026, more than double what it laid out the year before.

This is the heart of the quality question. NVIDIA’s returns on capital look spectacular partly because it barely deploys any, while Meta’s willingly denting its near-term returns to fund an AI build whose payoff is still unproven, a bet on itself that’ll define the stock for years.

Same coin, and yet one face is harvesting while the other is planting.

Two Wide Moats, Two Soft Spots

Planting or harvesting, both faces are well guarded, and each has one wall worth watching.

NVIDIA’s moat was never really the silicon, which rivals can eventually match. It’s CUDA and the stack of software and networking around it, the stuff that makes leaving painful once you’ve built on it. Even NVIDIA’s own risk factors say the quiet part out loud: its biggest customers are designing their own chips, and export rules already have it planning for zero data center compute revenue from China.

Meta’s moat is its social graph, 3.5 billion people who show up daily, a network rivals have burned years and fortunes failing to crack. Its weak spot is regulatory as much as competitive. The user base dipped a touch in early 2026 after an outage in Iran and a WhatsApp block in Russia, and the pressure around minors is now hardening into law: Australia bars under-16s from Facebook and Instagram, a world-first ban in force since December 2025, and France, Canada, Denmark, Malaysia, and several US states are weighing versions of their own. Meta also discloses that a bad outcome in its youth-safety lawsuits could be material.

What Links Them Is Also What Threatens Them

Here’s the catch, and it’s the whole reason the coin metaphor matters: the same deal that ties these two together ties their risks together, too.

NVIDIA sells to a small circle of hyperscale buyers, and Meta’s one of them. Should that circle pull back, NVIDIA feels it first, right at the front of the line.

Meta’s exposure runs the other way. It’s committed as much as $145 billion in a single year to infrastructure whose payoff hangs on AI products still finding their feet. That’s precisely the reason why the stock dropped when the number went up. Reality Labs piles on roughly $19 billion in annual operating losses.

Strip it all down, and both rest on one thing: steady demand for AI compute. That’s what makes owning both feel safer than it is. But if you flip the coin the wrong way, a real cooldown in AI spending could take both down at once.

Two Positions, One Trade

So back to that comfortable feeling of being diversified.

NVIDIA and Meta look like competitors, but they read more like two seats at the same table. NVIDIA’s the supplier: light on assets, heavy on cash, riding a shortage, and exposed to that shortage fading and to customers who’d rather build their own chips. Meta’s the buyer: a cash-rich ad business betting big, partly on borrowed money, that owning AI outright pays off. One gives you cleaner economics today with a bumpier ride; the other, a steadier core with a real capital-allocation gamble attached.

Neither’s better in a vacuum. They just suit different investors and different time horizons. The point isn’t to pick a face, it’s to see the whole coin clearly, from the filings instead of the headline of the week.

That’s exactly what Search10k is built to do: put any two companies side by side, in their own words, in about a minute.

| Want to run this yourself? Put any two companies head-to-head with Search10k’s side-by-side screener. Start a free trial or book a walkthrough. |

PRIMARY SOURCES

- NVIDIA. Fourth Quarter and Fiscal 2026 Results (Feb 25, 2026).

- NVIDIA. First Quarter Fiscal 2027 Results (May 20, 2026).

- NVIDIA. Form 10-K, fiscal year ended Jan 25, 2026 (SEC EDGAR).

- Meta Platforms. Fourth Quarter and Full Year 2025 Results (Jan 28, 2026).

- Meta Platforms. First Quarter 2026 Results (Apr 29, 2026).

- Meta Platforms. Form 10-K, fiscal year ended Dec 31, 2025 (SEC EDGAR).

Disclaimer: This article is for informational and educational purposes only. It is not investment advice, a research report, or an offer or solicitation to buy or sell any security. Statements of fact are drawn from the companies’ public filings and earnings releases, which are linked throughout and are historical in nature; past performance does not guarantee future results. Any interpretation or characterization of those facts is opinion, not a statement of fact. Forward-looking items, including NVIDIA’s and Meta’s capital-expenditure and revenue guidance, are the companies’ own forward-looking statements, are subject to the risks and uncertainties described in their SEC filings, and may differ materially from actual results. Readers should perform their own due diligence and consult a licensed professional before making any investment decision.